Frustration is something we all experience on a daily basis. Sometimes the internet lags, and the traffic is too slow, and the queues are too long, and the forms are too complicated.

While this frustration appears to be an inconvenience, it is actually an opportunity for entrepreneurs to create a convenient solution.

Convenience is defined as ‘a thing that contributes to an easy and effortless way of life.’ People are always looking for a product or service that minimizes cost, time, and effort, and they are willing to pay large amounts of money for it.

By identifying someone’s problem and creating a smart and convenient solution, you can generate a large income for yourself.

You might be asking yourself how important convenience is when it comes to business. After all, there are a hundred other things that you should be worrying about.

Well, convenience is critical to the customer experience, and it influences how your customer engages with your product or service.

It also guides the buying process and determines whether or not customers remain loyal to your brand. Simply put, customers are drawn to convenient products and services.

One market that is heavily driven by convenience is the mobile-phone market. As mobiles become more central to our daily routine, entrepreneurs have had to come up with mobile-oriented products and services that make our lives easier.

One service that stands out is M-PESA; a money transfer scheme that is much-loved in my home country of Kenya. Below we will look at the role M-PESA plays in bringing convenience to households and businesses across the country.

The M-PESA Model

Let’s start with your most pressing question; what is M-PESA?

M-PESA is a microfinance service and an SMS-based money transfer scheme, which allows registered users to make payments, deposit cash, transfer cash, withdraw cash, and borrow cash using inventive mobile phone technology.

The M in its name stands for Mobile, while Pesa is the Swahili word for money.

M-PESA was launched in 2007 as a joint venture between Vodafone and Safaricom, the latter being Kenya’s biggest mobile network operator. In the 8 years since its launch, M-PESA has spread to Tanzania, South Africa, Mozambique, Lesotho, Egypt, Afghanistan, India, Romania, and Albania.

The M-PESA service was created to reach the large ‘unbanked’ population, who had no access to financial services.

Even though banks have been asked time and time again to open up branches in rural locations, they have ignored this plea due to the fact it makes no business sense; most people who live in rural locations are poor, and their financial transactions are considered too small.

This disregard for the poorer members of society has left a huge number of Kenyans without bank accounts.

Cue in M-PESA, which operates at the micro-level that banks have ignored, providing convenient financial services to all members of society.

Why did M-PESA take off so fast?

To say that M-PESA is popular is understatement. M-PESA has achieved unprecedented acceptance, and it is considered to be the most successful mobile-phone money system in the world.

At the moment, M-PESA has over 20 million registered subscribers in Kenya alone, which is over 80% of the adult population. In the financial year that ended in March 2015, M-PESA generated Sh32.6 billion ($326 million) in revenue.

So how did it gain traction so fast?

1. Safaricom (which operates M-PESA) has a 67.4% market share in Kenya’s telecommunication market. Add onto that the fact that Kenyans have an inherent trust of Safaricom, and you have a large and willing customer base.

2. Over 80% of Kenyans own a mobile phone, and can therefore use M-PESA

3. M-PESA started as an experimental scheme, and it therefore run without strict regulation or restriction for the first few years. As you can imagine, this hands-off approach was heavily opposed by the banking industry which was afraid of losing profits.

4. Safaricom rolled out a brilliant distribution strategy for M-PESA. By quickly recruiting and training agents across the country, Safaricom ensured that it could start building strong relationships with customers.

To learn more about the economics of M-PESA, check out this insightful MIT Sloan and Georgetown University assessment.

Watch this M-PESA AD, I promise you’ll love it:

Is M-PESA a Bank?

As I’ve mentioned above, M-PESA allows you to deposit, transfer, withdraw, and borrow cash. These are all functions that are carried out by a bank, so using that line of thought; M-PESA should be classified as a bank.

Not quite. When you deposit funds in your M-PESA account, they are held in a ‘Trust’ across several commercial banks. This ‘Trust’ does not generate interest, and the money is not lent out to third parties. Simply put, any money you deposit cannot be accessed or used by anyone else, including Safaricom.

In this way, M-PESA avoids being classified and regulated as a bank. This means that if Safaricom ever went bankrupt (which is highly unlikely considering its profits), creditors would be unable to touch your money.

How M-PESA Works

REGISTER: If you own a Safaricom SIM-card (which almost all Kenyans own), you can register as an M-PESA user using your original I.D. You can register at any M-PESA outlet, which you will find at every other pharmacy, grocery store, kiosk, bank, and petrol station.

DEPOSIT: If you want to deposit money into your phone, head over to an M-PESA vendor/agent who will transfer the cash in your hand to e-float (virtual money) which is stored on your phone under your name.

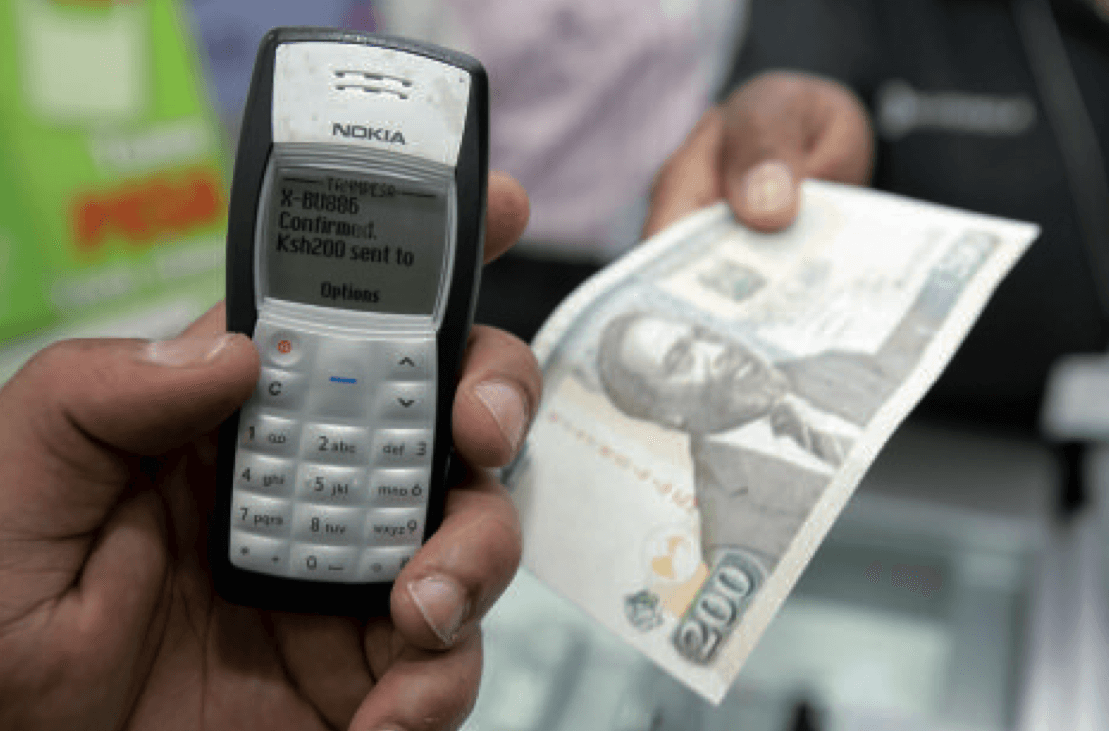

TRANSFER: If you want to transfer money to another person, go the M-PESA menu on your phone, select ‘send money’, and enter the desired phone number and money value. The money will be transferred instantly via a PIN-secure SMS text message.

“You are effectively texting money” Bob Collymore, CEO of Safaricom

WITHDRAW: If you want to withdraw cash, head over to an M-PESA vendor, and they will exchange the e-float on your phone to cash in hand.

Alternatively, you can withdraw cash using an ATM, as many ATMs have an integrated M-PESA function.

(picture source: africanbusinessmagazine.com)

FYI

1. You can hold money in your M-PESA account for as long as you want.

2. You can have a maximum account balance of Sh100000 ($1000).

3. Your maximum daily transaction value is Sh140000 ($1400), with a maximum of Sh70000 ($700) per transaction.

4. Your minimum withdrawal value at an M-PESA vendor is Sh50 ($0.5).

5. You will need to show your I.D whenever you deposit or withdraw money using a vendor.

6. You can transfer money to non-users; however, there will be a higher charge for that.

Other M-PESA services

M-PESA is not only used to deposit, transfer, and withdraw money, it can also be used for a variety of purposes:

1. Paying utility bills: electricity, water, garbage, and internet services

2. Buying goods: over 50,000 merchants in different sectors of the economy (e.g. petrol stations, taxis, hotels, clothes stores) accept M-PESA as a mode of payment

3. Paying your taxes

4. Fundraising: this has been of great help during disasters, such as the drought in Northern Kenya in 2011 and the Westgate terrorist tragedy in 2013

5. Paying salaries

6. Purchasing airtime

7. Accessing your commercial bank account

8. International money transfer: through partnerships with Western union, mHits, Post finance, Skrill, Sky Forex, World Remit, Xend Pay, and Xpress Money

9. Save and borrow money: M-Shwari is a banking product integrated into M-PESA. You can deposit money into your M-Shwari account where it will gain interest over time (up to 5% interest per annum). This is the perfect savings account for segments of the population who do not have a bank account.

As you continue saving your money, you will gain access to low-interest loans without the strict conditions of banks.

As you can see, there are no limits with M-PESA.

(picture source: venturesafrica.com)

Benefits of M-PESA

An overwhelming number of Kenyans say that M-PESA is fast, reliable, affordable, cheap, safe, and easy to use, especially when compared to other money transfer services.

M-PESA has managed to touch the lives of millions of people and businesses across the country, due to the following reasons:

- Convenience: There are 85,000+ vendors across the country, and you can therefore use M-PESA whenever you want, and wherever you like

- Low-technology: Even though the technology used to create M-PESA is advanced, it can be used on mobile phones with basic technology

- Time saving: You do not need to travel to a bank and stand in long banking lines anymore

- Low fees: There is no charge for depositing money, and the fees for transferring and withdrawing money are very low. To withdraw Sh1000 ($10) you will be charged Sh30 ($0.4), and to withdraw Sh70000 ($700) you will be charged Sh330 ($3.3)

- Ease of use: The M-PESA menu is simple and straightforward

- Flexibility: The M-PESA service can be used in a variety of situations, such as emergencies, payment collection, and even SACCOs

- Class-Less: M-PESA is accessible to all members of society, and no one is left out

- Safe: Transactions are protected by a PIN, and you can use M-PESA to carry cash instead of carrying a wallet full of money

- Regulated: M-PESA transactions are closely monitored by Safaricom to prevent money laundering

- Trained vendors: All M-PESA vendors are highly trained and closely supervised by Safaricom. This prevents delays and mistakes on their part.

Drawbacks of M-PESA

M-PESA is not a perfect model, and it does have its flaws. These include:

- Service interruption: During the last 8 years, the M-PESA service has been down one or two times due to issues with the Safaricom network. As you can imagine, these disruptions heavily impacted the actions of the average Kenyan. Thankfully, disruptions to the service are very rare.

- Criminal enterprise: Like any money platform, M-PESA can be used as a way to conduct scams, money laundering, and other shady enterprises. However, the system is advanced, regulated, and monitored, and this has worked to hamper the actions of criminal enterprise. You will also need to use your judgment; if a random person texts you and asks you to send them money, don’t do it!

- Inventory management issues: When you visit an M-PESA agent, they should have e-float and cash available for deposits and withdrawals respectively. However, if their inventory management is off, then they will be out of cash or e-float, which will delay your transactions. Thankfully, there are plenty of M-PESA vendors to use, and most are in close proximity to each other.

Final Verdict

When it comes to convenience, M-PESA scores high. This valuable service has dedicated itself to making the lives of Kenyans easier, by providing them with a financial service that they can take advantage of on a daily basis.

By spearheading the mobile-money revolution on the continent, M-PESA dominates a market that larger tech giants would sell their soul for. M-PESA is not just satisfactory and easy, it is outstanding and beneficial.

This type of service is what entrepreneurs should try and create; something that breaks down inconvenience barriers so that your customer’s life is much easier.

Before you leave, share this with your friends, family, and colleagues. Also drop me a comment and let me know what you admire most about M-PESA. And don’t forget to sign up to the newsletter for firsthand updates on new blog posts.

I hope you have a great week, and I’ll see you back next week.

Here’s one more beautiful M-PESA AD that you’ll love:

$1= $102 (30th Nov 2015)

Sounds like a great app that satisfies a needed demand. There are so many problems that need innovative thinkers to come up with new ideas to solve them. Thanks for sharing!

LikeLike

M-PESA definitely meets the demands of the average Kenyan. And I do agree with you when it comes to the need for innovative thinkers!

LikeLike

M-pesa is unique for Kenya, It meets the unmet demand.

Companies who think from a consumers perspective are successful

LikeLike

The video’s are so beautiful done and it shows how beautiful your country is. It’s a great service.

LikeLike

I love the videos too; Kenya is extremely beautiful. Thanks for checking the post out 🙂

LikeLike

What a brilliant idea! I’m impressed that it caught on so quickly and that millions of folks are using it in Kenya. What a great tool to help with financial transactions!

LikeLike

It’s definitely amazing Elizabeth 🙂

LikeLike

Nice to see an app that has been designed to meet a genuine need and is working so well

LikeLike

Thanks Mike!

LikeLike

In this day and age it’s all about convenience and efficiency and I think M-pesa is doing all that in one go. What a wonderful service.

LikeLike

I definitely agree Miranda!

LikeLike

you inspire me @Davina

LikeLike

Thank you Jerry 🙂

LikeLike

Well laid out article that explains to a layperson anywhere around the world how M-Pesa works.

You’ve pretty much covered everything that needs to be known about the app.

What I need to add is that the app is now used around the world as a model for phone based money apps.

The app has also garnered many international awards.

LikeLike

Thank you Gitura 🙂 And thanks for the addition; this is definitely a revolutionary app..

LikeLike